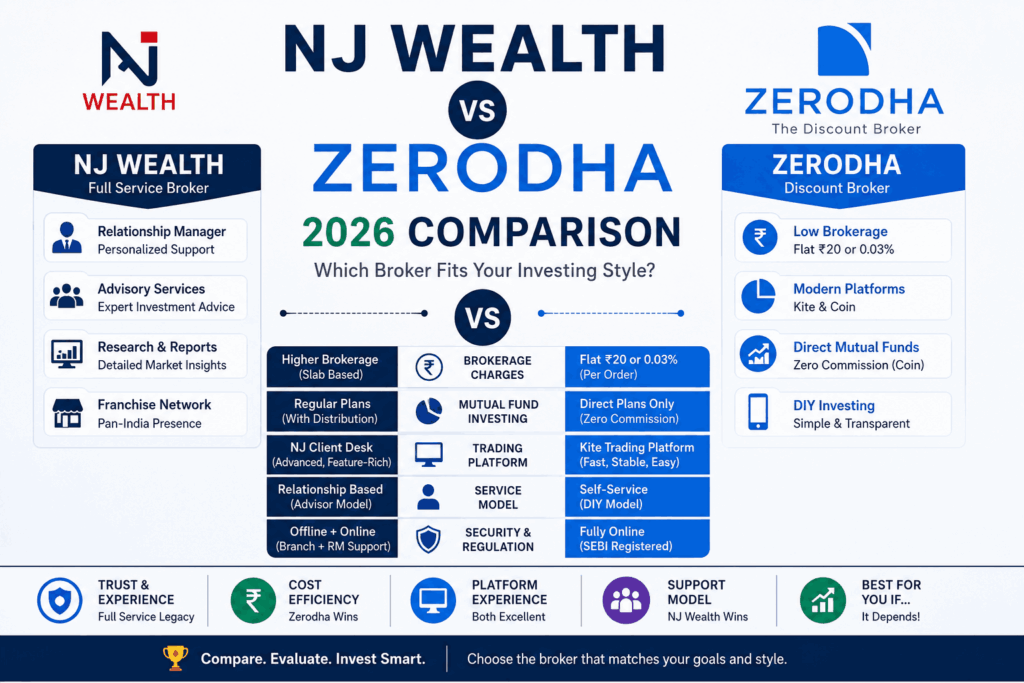

If you are trying to decide between NJ Wealth and Zerodha, you are not really comparing two of the same thing. These are two genuinely different business models that happen to both let you buy and sell financial products. One is a 25-year-old advisor-led distribution network with 33,000+ franchises serving over 1 crore mutual fund folios. The other is a 16-year-old discount broker that single-handedly reshaped how Indians trade stocks.

The right choice between NJ Wealth vs Zerodha is not about which broker is “better” in absolute terms. It is about which model fits the way you actually want to manage money. Do you want a person who guides you through every decision and earns a commission on the products you buy? Or do you want a do-it-yourself platform that charges almost nothing but expects you to make your own choices?

This comparison breaks both brokers down across every dimension that matters – brokerage charges, account costs, platforms, mutual fund pricing structures, security and regulation, the cost over a 10-20 year horizon, and the underlying business model that shapes everything else. By the end, you should know which one fits you – and crucially, which one would slowly drain your wealth if you picked it for the wrong reason.

NJ Wealth and Zerodha are not competitors in the traditional sense. They serve fundamentally different needs – advisory-led financial planning vs DIY low-cost trading. Picking the wrong one for your style is more expensive than picking the right one and switching later.

Who are NJ Wealth and Zerodha?

NJ Wealth – the largest mutual fund distributor in India

NJ Wealth was founded in 2000 by Niraj Ravindra Choksi and is headquartered in Surat, Gujarat. Over the last 25 years, it has built what is arguably India’s largest distribution network for financial products – a partner-led model with over 33,000 registered franchises, sub-brokers, and Independent Financial Advisors (IFAs) operating across nearly every district in India.

The core idea behind NJ Wealth is human distribution at scale. Rather than selling financial products through a single app or website, NJ Wealth equips thousands of partners – typically Chartered Accountants, financial planners, mutual fund advisors and sub-brokers – with the tools, technology and product range needed to serve their own local clients. Those partners earn commissions on the mutual funds, insurance, fixed deposits, bonds and equity products they bring in. NJ Wealth has built a partner-management technology layer (NJ Partner Desk) that runs this network.

The brokerage arm – NJ Wealth’s stock-broking and demat business – is operationally a smaller part of the overall enterprise. The mutual fund distribution business is the giant. NJ Wealth’s MF folio base is rumoured to be over 1 crore (10 million), which is enormous by any standard. Stockbroking is a complementary service, not the main act.

Zerodha – India’s largest discount broker

Zerodha was founded in 2010 by Nithin Kamath and is headquartered in Bengaluru. It pioneered the flat-fee discount broking model in India – Rs. 20 (or 0.03%) per executed order, regardless of trade size – and forced the entire industry to rebuild around that price point. Most discount brokers in India today are direct descendants of the model Zerodha created.

As of 2026, Zerodha has approximately 68 lakh active clients on NSE, putting it second only to Groww in market share. The Kite platform (web and mobile) is widely regarded as the gold standard among Indian trading apps for reliability and execution speed. Beyond Kite, Zerodha has built a broader ecosystem: Coin for direct mutual funds, Varsity for trader education, Kite Connect API for algorithmic trading, and partnerships with third-party tools like Sensibull, Streak and Smallcase.

Zerodha’s stated philosophy is simple – sell DIY tools, not advice. The company famously does not have a research desk producing buy/sell recommendations, does not assign relationship managers, and does not sell regular-plan mutual funds. The trade-off: investors who want personal hand-holding will not find it at Zerodha.

NJ Wealth vs Zerodha at a glance

| Attribute | NJ Wealth | Zerodha |

|---|---|---|

| Founded | 2000 by Niraj Ravindra Choksi | 2010 by Nithin Kamath |

| Headquarters | Surat, Gujarat | Bengaluru, Karnataka |

| Broker Type | Full-service / Distributor-advisor | Discount broker |

| Active clients (NSE) | Not separately disclosed (large MF folio base) | ~68 lakh |

| MF folio base | Largest MF distributor in India (1+ crore folios) | MF via Coin platform |

| Distribution model | Partner-led: 33,000+ franchises and sub-brokers | Direct-to-consumer; online only |

| Mutual fund plans sold | Regular plans (commission embedded) | Direct plans (zero commission) |

| Primary trading platform | NJ Client Desk (web) | Kite (web + mobile) |

| Mobile-first app | Less mature; web-led | Yes – Kite mobile is flagship |

| Best for | Advisor-led investors, mutual fund-heavy portfolios | DIY traders, low-cost active investing |

NJ Wealth vs Zerodha: brokerage and charges compared

This is where the two brokers diverge most sharply. NJ Wealth charges a percentage-based brokerage that is typical of full-service brokers. Zerodha charges a flat fee per order. The implications for your wallet are very different depending on your trade size.

| Charge | NJ Wealth | Zerodha |

|---|---|---|

| Account opening | Rs. 300 | Rs. 200 |

| Trading AMC | Rs. 250 per year | Not applicable (built into demat AMC) |

| Demat AMC | Free (Rs. 354 DP charge typically refundable) | Rs. 300 per year |

| Equity Delivery brokerage | 0.10% to 0.20% of trade value | Free (Rs. 0) |

| Equity Intraday brokerage | 0.01% to 0.02% of trade value | Lower of Rs. 20 or 0.03% per order |

| Equity Futures brokerage | 0.01% to 0.02% of trade value | Lower of Rs. 20 or 0.03% per order |

| Equity Options brokerage | Rs. 10-20 per lot | Rs. 20 flat per order |

| Currency Futures | 0.01% to 0.02% | Rs. 20 flat per order |

| Currency Options | Rs. 10-20 per lot | Rs. 20 flat per order |

| Commodity | 0.01% to 0.02% | Rs. 20 flat per order |

| Mutual Funds | Regular plans only (commission in NAV) | Direct plans, Rs. 0 commission |

| Call & Trade | Available | Rs. 50 per call |

| DP charges (per sell) | Standard CDSL + broker fee | Rs. 13.50 + 18% GST |

What the brokerage gap looks like in real rupees

Numbers in a table can be hard to internalise. Here is the same comparison framed as actual rupee cost on typical trades. These figures use NJ Wealth’s standard brokerage rates and Zerodha’s published flat fees, plus an approximation for statutory charges (which are identical at both brokers).

| Trade Scenario | NJ Wealth Cost | Zerodha Cost |

|---|---|---|

| Rs. 1 lakh delivery buy + sell | ~Rs. 300-400 (0.1-0.2% x 2) | ~Rs. 24-50 (DP + statutory) |

| Rs. 5 lakh delivery buy + sell | ~Rs. 1,500-2,000 | ~Rs. 25-50 |

| Rs. 1 lakh intraday round trip | Rs. 20-40 + statutory | Rs. 40 + statutory |

| 1 lot Nifty options round trip | Rs. 20-40 brokerage | Rs. 40 brokerage |

| 50 F&O orders / month | ~Rs. 1,000-2,000 / month | Rs. 1,000 / month |

| 100 F&O orders / month | ~Rs. 2,000-4,000 / month | Rs. 2,000 / month |

On a Rs. 5 lakh equity delivery round-trip, NJ Wealth’s brokerage runs roughly 30x higher than Zerodha’s. On intraday and F&O, the gap is much narrower – because NJ Wealth’s percentage rates on those segments are actually quite competitive. The big swing is on delivery.

Why NJ Wealth’s percentage model hurts delivery investors most

If you are an equity delivery investor – someone who buys stocks and holds them for months or years – NJ Wealth’s 0.10-0.20% brokerage is substantially more expensive than Zerodha’s free delivery. The math compounds: on a Rs. 10 lakh long-term portfolio over 10 years with 20-30 transactions, NJ Wealth’s brokerage cost can run into Rs. 50,000-1,00,000 in extra fees. Zerodha would charge you near-zero on the same transactions.

For active intraday and F&O traders, however, the cost gap narrows significantly. NJ Wealth’s 0.01-0.02% intraday brokerage, applied to a small-ticket trade, often works out close to Zerodha’s flat Rs. 20. The advantage of NJ Wealth here is the inclusion of advisory services on top – the fee is not just brokerage, it is also bundled human guidance.

Trading platforms and tools compared

The platforms are where the discount-vs-full-service divide becomes most visible. Zerodha is mobile-first and DIY-first; NJ Wealth is web-first and advisor-mediated.

| Feature | NJ Wealth | Zerodha |

|---|---|---|

| Web platform | NJ Client Desk – browser-based, no install | Kite web – fast, lightweight |

| Mobile app | NJ E-Wealth Account; functional but limited | Kite mobile – flagship, frequent updates |

| Desktop terminal | Not core to offering | Kite web is the desktop terminal |

| Charting | Basic with technical indicators | Advanced – TradingView integration available |

| Order types | Market, Limit, SL, basic conditional | Market, Limit, SL, SL-M, GTT, AMO, BO, CO |

| API / Algo trading | Limited | Kite Connect API – the industry standard |

| Third-party integrations | Limited | Sensibull, Streak, Smallcase and 30+ others |

| Education | Advisor-led; physical training | Varsity – the deepest free education library in India |

Zerodha Kite

Kite is consistently rated among the best trading platforms in India. It is built around speed, simplicity and reliability – the things that matter most when you are placing trades during volatile sessions. Order execution latency is among the lowest in the industry. The mobile and web versions share the same backend, so your watchlists and positions sync seamlessly. For active traders, Kite is widely considered the benchmark every other broker is measured against.

NJ Wealth Client Desk

NJ Client Desk is a browser-based platform that runs without installation. Its strength is the consolidated view it offers across mutual funds, insurance, fixed deposits, bonds and equity – a holistic family-finance dashboard rather than a pure trading terminal. For a long-term investor primarily focused on mutual fund SIPs with occasional equity transactions, this consolidated view is genuinely useful. For an active trader, it lacks the speed, advanced order types and third-party integrations Kite offers.

Mutual funds: the most important difference

If you are buying mutual funds through NJ Wealth or Zerodha, there is a structural difference that will affect your wealth more than any other choice in this comparison. NJ Wealth sells Regular plans (with embedded distributor commissions). Zerodha Coin sells only Direct plans (with no commissions). The difference seems small in any one year. Over 20 years, it is enormous.

| Aspect | NJ Wealth (Regular plans) | Zerodha Coin (Direct plans) |

|---|---|---|

| Expense ratio | Higher (1.5% to 2.25% typically for equity) | Lower (0.5% to 1.00% typically for equity) |

| Distributor commission | Embedded in expense ratio – paid to NJ partner | None – direct from AMC |

| Annual cost drag | Roughly 1.0% per year extra | Lower expense ratio = higher NAV growth |

| 20-year cost on Rs. 5 lakh MF | Approximately Rs. 12-15 lakh in lost compounding | Baseline – higher terminal value |

| Advisor relationship | Yes – human partner / sub-broker | None – self-directed |

| Suited for | Investors who want hand-holding and are comfortable paying for it | DIY investors who can pick funds independently |

A 1% per year difference in mutual fund expense ratios compounds to roughly 20-25% less wealth over 25 years. For a long-term equity SIP investor, this is the single biggest cost difference between NJ Wealth and Zerodha – far bigger than the brokerage difference on equity trades.

Why NJ Wealth still sells regular plans in 2026

NJ Wealth’s entire business model is built on partner distribution – 33,000+ franchises whose income depends on the trail commission embedded in regular-plan expense ratios. Direct plans would cut that income line entirely. So NJ Wealth has not added direct plans; its partners would lose their livelihood.

If you genuinely value the human advisor relationship – and many investors do, especially those approaching retirement or managing complex family portfolios – paying that 1% per year for personalised guidance can be worth it. If you do not need or use the advisor relationship, you are paying for a service you are not consuming. The question is honest self-assessment.

Security, regulation and trustworthiness

Both NJ Wealth and Zerodha are SEBI-registered intermediaries with full regulatory standing. NJ Wealth’s stockbroking arm is a SEBI-registered stockbroker; NJ Wealth itself is also registered as an Investment Adviser (IA) and Mutual Fund Distributor (MFD). Zerodha is a SEBI-registered stockbroker.

The standard three-pillar protection applies equally to both:

- Securities held in your name. Whether you open a demat account with NJ Wealth or Zerodha, your shares and mutual fund units are held in CDSL or NSDL under your own PAN. Even if either broker shut down, your holdings stay safe and can be transferred.

- Client funds segregation. Both brokers must keep client funds in separate bank accounts per SEBI norms, with daily settlement true-ups.

- Investor Protection Fund coverage. NSE and BSE both maintain Investor Protection Funds covering eligible claims in case of broker default.

Operationally, Zerodha has been profitable, debt-free, and publicly committed to staying private with no PE money. It is the most financially conservative discount broker in India. NJ Wealth has been operating profitably for 25 years and is the largest distributor in the country. Both are structurally safe businesses. There is no meaningful safety advantage on either side.

Who should pick NJ Wealth – and who should pick Zerodha?

Pick NJ Wealth if you…

- Want a human advisor relationship rather than a self-service app

- Are approaching retirement or managing complex family financial planning

- Value face-to-face meetings with a local sub-broker or financial planner

- Want one platform for mutual funds, insurance, fixed deposits and other products together

- Are willing to pay slightly more in commissions for guidance and hand-holding

- Live in a tier-2 or tier-3 town where NJ Wealth’s franchise network is strong

- Do not trade equity actively – your needs are mostly long-term mutual funds and FDs

Pick Zerodha if you…

- Are comfortable making your own investment decisions

- Trade equity, F&O or commodities actively – or plan to

- Want the lowest possible brokerage cost on every trade

- Buy mutual funds and want direct plans (saves 1% per year over regular plans)

- Value modern technology – clean mobile app, fast execution, third-party tool integrations

- Want algo trading APIs (Kite Connect) or use platforms like Sensibull, Streak

- Are willing to do your own research using Varsity, news sources and screeners

Most investors will fit clearly into one camp or the other. The few investors who genuinely need both – personalised advice for long-term planning, plus low-cost active trading – sometimes open accounts at both. There is no rule against having two demat accounts.

Pros and cons of each broker

NJ Wealth – pros

- Strong human advisor relationship through partner franchises

- Consolidated view of mutual funds, insurance, FDs and equity in one platform

- Largest mutual fund distribution network in India – tier-2 and tier-3 reach

- 25-year track record – mature business, financially stable

- Goal-based financial planning support built into the model

- DP charges typically refundable through the broker incentive structure

- Useful for families and individuals who need help making decisions

NJ Wealth – cons

- Equity delivery brokerage at 0.10-0.20% is significantly higher than discount brokers

- Only sells regular-plan mutual funds – higher expense ratio than direct plans

- Trading platform feels dated compared with Kite or Groww

- Limited algo trading and API support

- Less mobile-first – app experience trails newer platforms

- Brokerage charges are flexible and partner-negotiated – less transparent than flat fees

- Smaller third-party integration ecosystem

Zerodha – pros

- Free equity delivery – meaningful for long-term investors

- Flat Rs. 20 per order on intraday and F&O – industry standard

- Kite platform is fast, reliable and continuously improved

- Direct mutual funds via Coin – saves 1% per year in expense ratio

- Kite Connect API is the most-used algo trading API in India

- Varsity provides the deepest free trader education in India

- Strong third-party tool ecosystem (Sensibull, Streak, Smallcase)

- Debt-free, profitable, and committed to staying private

Zerodha – cons

- No relationship manager or human advisor

- Rs. 300 annual demat AMC – higher than some discount brokers (Groww, Dhan)

- Mutual funds live in a separate app (Coin) rather than alongside trading

- No research reports or stock recommendations

- Call & Trade costs Rs. 50 – higher than the m.Stock or Dhan equivalents

- Customer support is slow during peak market hours

- Not the best fit for absolute beginners who need hand-holding

2026 updates affecting both brokers

Two regulatory and market changes in 2025-2026 affect investors at both NJ Wealth and Zerodha:

- Higher STT on F&O (April 2026): The government raised Securities Transaction Tax on futures (from 0.02% to 0.05% on sell side) and on options (from 0.10% to 0.15% on sell premium). These are statutory charges – identical at NJ Wealth and Zerodha – and affect any F&O trader’s cost structure regardless of broker.

- Updated capital gains tax framework: Long-term capital gains on equity are now taxed at 12.5% on gains above Rs. 1.25 lakh per year. Short-term gains are taxed at 20%. The tax treatment is identical regardless of which broker you used – the broker is just the order-placement channel.

- Continued evolution of broker offerings: Zerodha has continued to refine Kite (especially mobile) and Console. NJ Wealth has invested in upgrading its partner-management technology but the consumer-facing platform has seen smaller updates. The directional trend – discount brokers gaining client share, full-service brokers focusing on advisory value – has continued through 2026.

Frequently Asked Questions

Q1. Which is better between NJ Wealth and Zerodha for beginners?

It depends on your style. If you want personal guidance from a human advisor and prefer face-to-face support, NJ Wealth is the better fit through its 33,000+ franchise network. If you are comfortable learning independently using YouTube, Varsity and online research, Zerodha is meaningfully cheaper and more modern. Most absolute beginners are better off with Groww or Zerodha for the lower friction; those who want hand-holding gravitate to NJ Wealth or local IFAs.

Q2. What is the actual brokerage difference between NJ Wealth and Zerodha?

For equity delivery: NJ Wealth charges 0.10-0.20% of trade value, while Zerodha charges Rs. 0 (free). On a Rs. 1 lakh delivery trade, that is Rs. 100-200 at NJ Wealth versus zero at Zerodha. For intraday and F&O, the gap is much narrower – NJ Wealth’s 0.01-0.02% intraday brokerage on a typical trade often works out similar to Zerodha’s flat Rs. 20.

Q3. Does NJ Wealth offer direct mutual funds like Zerodha Coin?

No, NJ Wealth sells only regular-plan mutual funds. Regular plans have higher expense ratios (about 1% per year higher than direct plans) because they include distributor commission. Zerodha Coin sells only direct-plan mutual funds. Over 20-25 years of SIP investing, the difference compounds to roughly 20-25% less terminal wealth in regular plans.

Q4. Is NJ Wealth safer than Zerodha?

Both are SEBI-registered and equally safe under the regulatory framework. Your shares are held in CDSL or NSDL under your PAN at both brokers. Client funds are segregated at both. Investor Protection Fund coverage applies at both. There is no meaningful safety advantage on either side. Both businesses have been operating profitably for many years.

Q5. Can I trade F&O on NJ Wealth?

Yes, NJ Wealth supports equity futures, equity options, currency futures, currency options and commodity trading. The brokerage on these segments is 0.01-0.02% (futures/commodities) or Rs. 10-20 per lot (options) – generally competitive with discount brokers. The trade-off is that the trading platform (NJ Client Desk) is less advanced than Zerodha Kite for active F&O trading.

Q6. What are NJ Wealth’s account opening and AMC charges?

NJ Wealth charges Rs. 300 for account opening (demat + trading) and Rs. 250 per year as trading AMC. Demat AMC is technically free, but there is a Rs. 354 DP charge (which is typically refundable). Zerodha charges Rs. 200 for account opening and Rs. 300 per year as demat AMC.

Q7. Can I switch from NJ Wealth to Zerodha or vice versa?

Yes. You can transfer your demat holdings from one broker to another using a DIS (Delivery Instruction Slip) or the CDSL Easiest portal. There may be a transfer-out charge from your existing broker (typically Rs. 20-50 per scrip or 0.5% whichever lower). For mutual funds, you can simply stop SIPs at one broker and start new SIPs at the other – the existing units stay in your folio.

Q8. Does NJ Wealth offer a mobile app like Zerodha Kite?

NJ Wealth has an NJ E-Wealth Account app, but it is less polished and feature-rich than Zerodha Kite. Active traders generally prefer Kite’s mobile-first experience. NJ Wealth’s primary platform is the web-based NJ Client Desk, which works on browsers across desktops and mobile.

Q9. Which broker is cheaper for long-term equity investing?

Zerodha is significantly cheaper for long-term equity investing because equity delivery is free. NJ Wealth charges 0.10-0.20% on every delivery transaction, which adds up over a long-term portfolio with periodic buying. Over 10-20 years of regular investing, Zerodha can save you tens of thousands of rupees in brokerage versus NJ Wealth – before even counting the direct vs regular mutual fund cost difference.

Q10. Which is better for mutual fund SIPs – NJ Wealth or Zerodha Coin?

If you want a human advisor to help you pick funds and rebalance your portfolio, NJ Wealth (regular plans) makes sense – you are paying for the relationship. If you are confident picking funds yourself and want the lowest cost, Zerodha Coin (direct plans) is structurally better – direct plans have lower expense ratios and compound to materially higher wealth over 15+ years. The 1% annual cost difference is the single biggest financial decision in this comparison.

Final verdict: NJ Wealth vs Zerodha

The honest answer to NJ Wealth vs Zerodha is that they serve different investor needs, and the comparison is less about which is better and more about which is better for you.

Three takeaways from this comparison:

- If you trade actively or invest in equity delivery, Zerodha wins decisively. Free equity delivery, lower per-order F&O cost, more reliable platform, more powerful tools. The cost advantage is real and compounds over years. For DIY traders and self-directed equity investors, Zerodha is the clearly better choice.

- If you need a human advisor for financial planning, NJ Wealth still makes sense. The 33,000+ franchise network reaches tier-2 and tier-3 India in ways online-only platforms cannot. For investors who genuinely use advisory services and value face-to-face support, the higher commissions are paying for a real human relationship – not nothing.

- On mutual funds, the direct-vs-regular gap matters most. If you can pick your own mutual funds with reasonable confidence, Zerodha Coin’s direct plans will compound to 20-25% more wealth than NJ Wealth’s regular plans over a 25-year horizon. This is the single biggest financial decision in this comparison.

Pick NJ Wealth if you actually use – and value – the advisor relationship. Pick Zerodha if you are confident making your own decisions. The wrong choice does not cause immediate damage; it slowly drains wealth over decades. The right choice does not feel like a triumph; it just quietly compounds in the background.

Neither broker is universally better. The right broker is the one whose model matches the way you actually invest – not the one your friend uses, and not the one with the slickest marketing.